It’s not a secret to anyone in the food industry that a few years ago, plant-based products and alternative protein were all the hype. However, two years down the road, investment interest in the field has plummeted, the excitement has faded, and many products and companies discontinued due to lack of commercial success. Is this a failure or are we just past a period of over-hyping that has now gone back to a healthy organic growth? So what should this whole segment learn from it?

Below I’m writing some experience-based takeaways that I personally believe to be some of the major issues and learnings we should be aware in the future.

Takeaway #1: “Get-rich-fast” thinking doesn’t belong in food-tech

The plant-based sector has been labeled in the past year as a “category failure” and now it’s mostly a topic that investors don’t want to get close to. The big issue is not the past two years, but the years before, where the industry was invaded by Venture Capital firms that treated the whole investment case as a software company, expecting unrealistic valuation returns in a few years, disregarding any sanity checks from any experienced professional from the food industry. When everyone is rushing to get good deals, who has time for proper technical DDs anyway?

So what’s the problem? Let's get some of the points down here:

> It takes years to develop a good food product. No, we can’t just AI-high-throughput sensorial testing of people experiencing a meal.

> It takes years to make sure something new that you put in your mouth is safe and nutritiously sound.

> It takes years to scale a good product and process from lab scale to producing it in thousands of tons consistently. It’s just a manufacturing and real-world logistics problem.

> It takes years after you accomplished everything above to actually break even from the large investments made.

So how does this make sense to a VC fund when you put the numbers in reality? It doesn’t, and that’s exactly what happened when all the hype has subsided. Does this mean we should stop investing in plant-based? Not even a little bit. But we need blended finance that accounts for longer-term returns. A great food product will return stable profits over decades, not a hyper-exponential growth in 2 years like a cloud-hosted SaaS product.

Takeaway #2: When it comes to food, shipping too fast can actually hurt you

Competent entrepreneurs and product managers out there know the drill: following the philosophy of “The Lean Startup” by Eric Ries, you should ship a product as soon as you can, and then use that as a test to discover what actually matters to your customers, proceeding to develop the product to match the exact needs customers need, not the ones they say they want. The problem with applying this too literally to food products in the plant-based sector comes at a cost though:

It takes one single 4€ purchase for a consumer to try a bad product and say “I’ve tried plant-based products, they’re horrible” and never buy it again.

Consumers are relentless when it comes to food. They expect a fantastic product from day 1, and will be quite reluctant to give you a second chance. On top of that, your competitors can actually hurt you and vice-versa, because a consumer can easily look beyond a brand as just put your product in a box of “I don’t like these types of products”. As if this wasn’t enough of a challenge, the only real feedback loop you might have is the number of repeated buys for your products. Other than that, it’s highly difficult to get any hard data about what are the properties or features of your product that prevent or enable those repeated buys (unless of course we go into surveys and focus groups, which is still not real world behaviour data, but it’s really the best we can get).

Success in this industry relies on delivering good products from day 1, and do this consistently. This requires years of commitment, a passion for the mission rather than fast money, consistently delivering on progress and scale-down production costs so the product is as cost-competitive as possible. What do you gain on this? Customer retention and loyalty. Food evokes feelings, and positive feelings are addictive. If a product delivers on this, the repeat buys just keep coming. We all have food products we are unshakeably loyal to, because we know they taste good, are good for us, are affordable, the kids like it, we align with the brand mission, etc.

Takeaway #3: Price-parity is nonsensical if we don’t talk about government subsidies

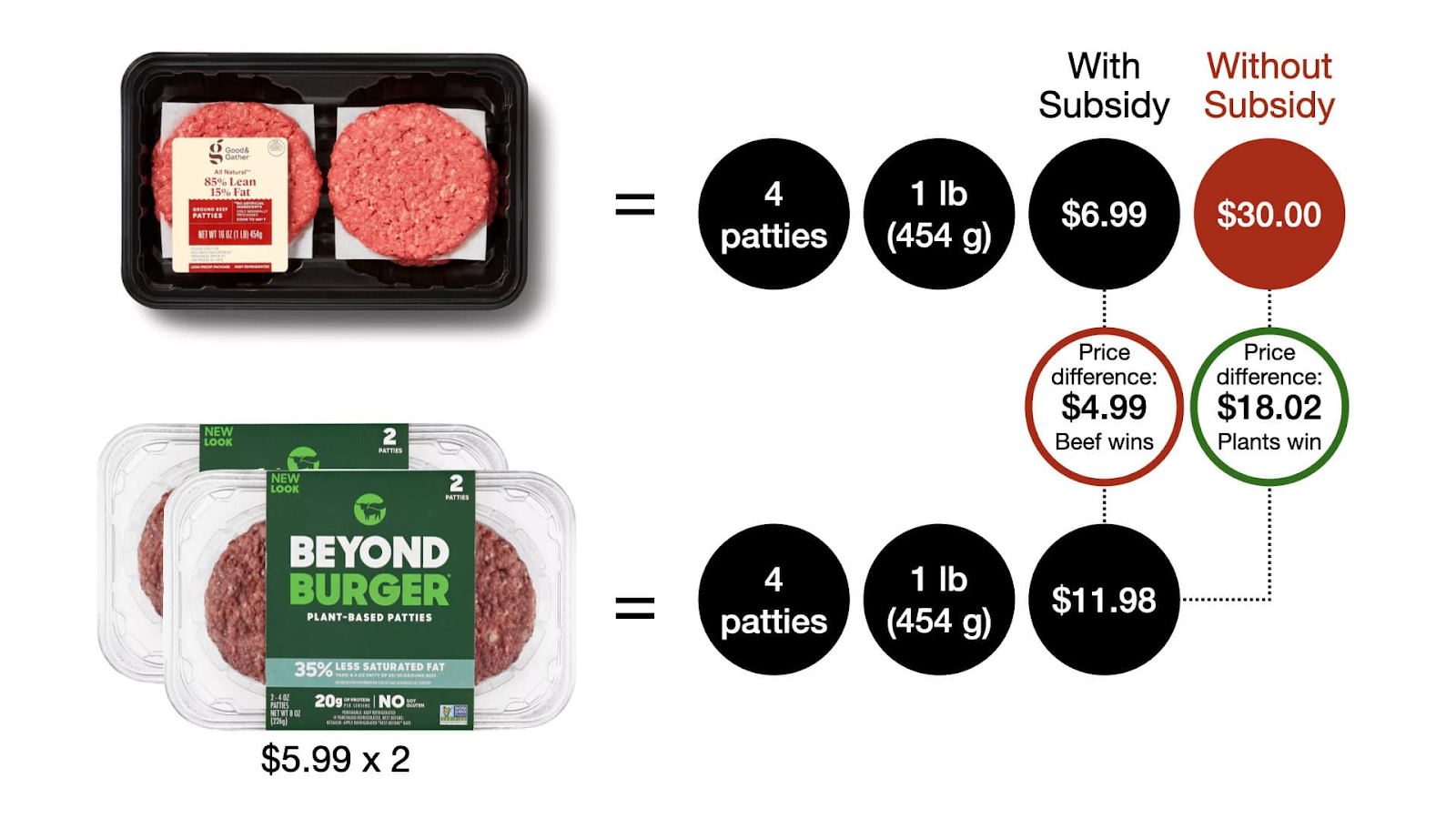

Every technology and product on the alternative protein and plant-based sector gets challenged with the key decision point for consumers and investors: how is the price when compared to the animal product counterpart? Consumers are not prepared to pay large differences, and even if a small subsegment is, without price-parity with meat there will never be enough volumes sold to create the real impact these products can create. So who receives the responsibility to reach low production costs? The creators, engineers, scientists behind the production methods, who need to make them more efficient, with less expensive equipment, at a less-than-massive scale that equates with sales volumes. But is the question really that technology is too young and efficient?

Cattle is mostly fed with edible crops (grains, soy, etc). To produce beef, we need about 25 kg of feed for each kg of edible meat. So how can this still be more cost-efficient than using that same crops directly for making a plant-based meat analogues? Looking into articles such as this one from Vegconomist shows us the reality that the real cost of producing meat is much higher than what consumers are paying. The meat bought at a supermarket is a highly subsidized product, and without government subsidies it would cost about 4 times more. And at the end of the day, where do these subsidies come from? (drumroll) Taxpayers money of course.

Source: Vegconomist, author: Lynette Kucsma

So, of course at a micro-scale the pressure goes to the startups and small companies developing breakthrough technologies, but the real issue is a distribution of funds at a governmental, pressured by corporate lobbies that will strongly oppose a change in the status-quo. The whole industry (investors included) needs an organized approach to tackle this issue, instead of passively conforming to play a rigged game. Only then can we see true change and fairness in price-parity.

Takeaway #4: The alternative protein segment is still immature and noisy

The advent of technologies and products within alternative and plant-based protein is exciting and still full of novelty. The downside is that innovation frontrunners are often small companies and startups that do not have the muscle power needed to penetrate the FMCG market. These small companies are then also using processes and often ingredients which the industry experts are not familiar with. In addition to the above, the influx of investors in the field has been mostly based on Venture Capital firms that are too prone to over-hyped business cases and valuations, and lack access to the right tools and competence for proper technical due-dilligence, or on the other side, industry- and market-savy corporations that then again lack the competence to understand the new technologies and offers and ask the right questions. This combination of loud boasting and uninformed hearing leads to many awkward movements in the market, which feedbacks again to a whole lack of trust in the industry and its driving players.

Examples of this can be anything from meat industry experts being seen as major value additions to commercializing cultured-meat products; companies with long competence in isolating plant and animal proteins believing they are able to equally scale fermentation-based protein production processes; or just early-stage startups receiving larger investments than other more mature counterparts, seemingly based on the ability to boast better financial numbers that are only possible due to a lack of real-world testing.

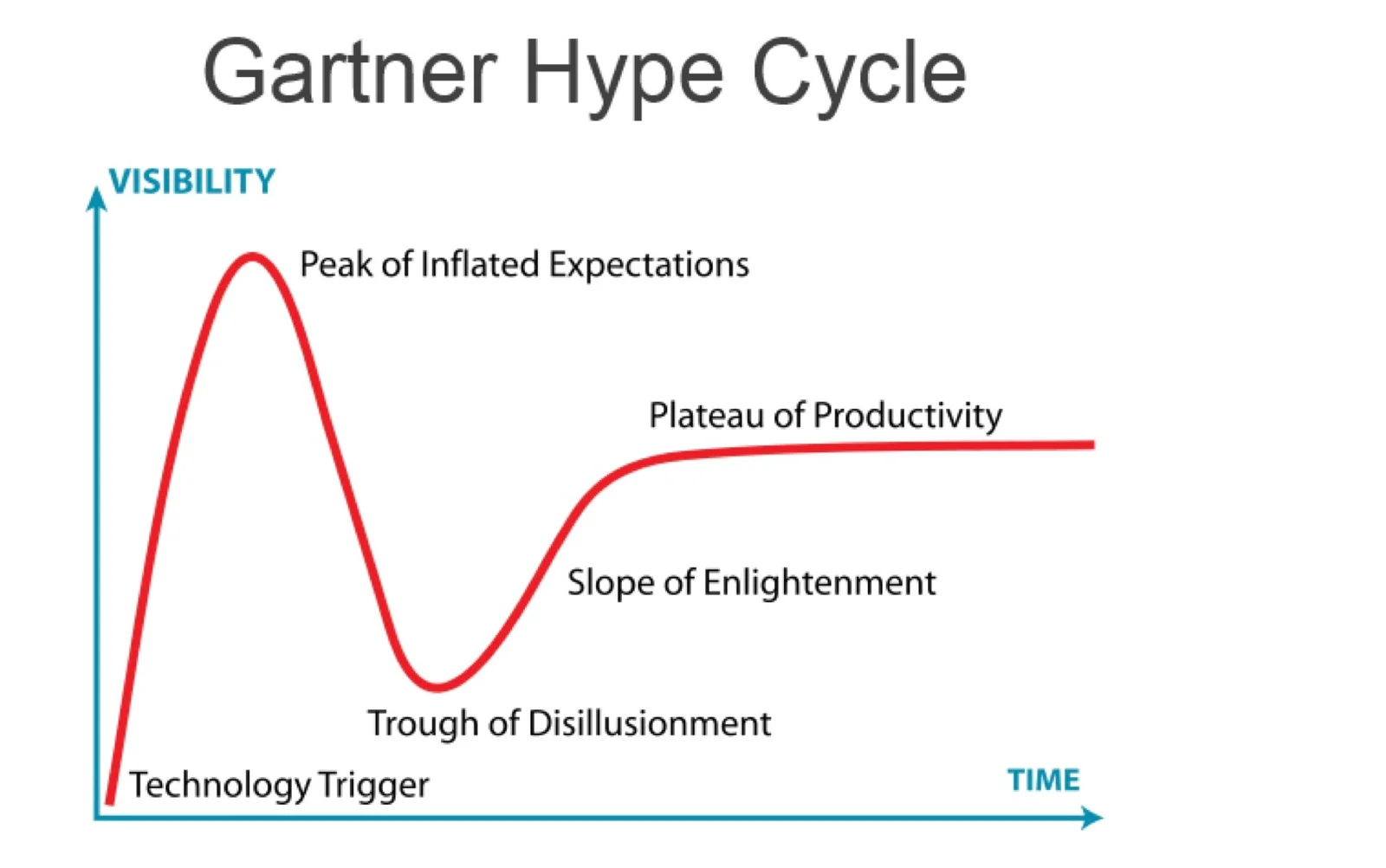

In general this is an issue that stability and maturity is achieved with enough time and enough trial-and-error. We’re going through a classic Gartner Hype Cycle in which 2022 saw the “Peak of Inflated Expectations” in the plant-based and alternativ protein sector, and through ups and downs we are approaching a stable plateau of development and real-world impact.

At the end of the day, changing the food system as we have today to drastically lower its carbon emissions and feed the whole population in a healthy way is something humanity needs to collaborate on. The cost of not doing this is eventually a drastic collapse of our capacity to grow crops, leading to widespread famine and war. The good news is, we have all the solutions we need. Now, we need a concerted effort of innovation actors, governments and funding bodies to drive unity in better products and nudge a change in diets through better consumer habits. Not the least, we also need to rethink the attitude of throwing the responsibility to the small companies that are already working day and night to make a difference in their relatively small radius of influence.

Author: Paulo Teixeira, PhD